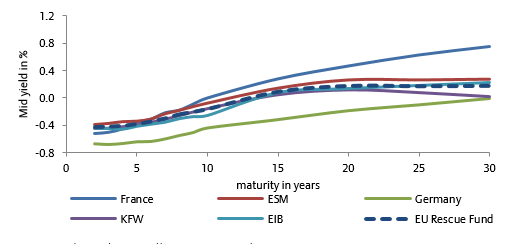

Prefer ultra-long bond financing over perpetual bonds (or consols). When it comes to question whether the fund should be partly financed with perpetual bonds, we think this would be a risky strategy. For one, perpetual bonds may not meet ECB’s eligibility criteria. Moreover demand for perpetual bonds is usually limited as the risk balance for the investor is skewed to his disadvantage, as the investment can only be retrieved if the bond is sold in the secondary market or gets called. Perpetual sovereign bonds do not currently exist in the Eurozone. It is not sure they would fly. The market acceptance would be a major uncertainty. A failed issuance would be a disastrous signal for the EU and Eurozone financial stability, and could destroy much of the positive sentiment related to the creation of the fund. If one really wants to use ultra-long maturities (be it for intergenerational equality or other reasons – even though the ECB can only buy debt with maturities up to 30 years), one should rather aim for emissions in the 50-100 years segment. Past issuances of ultra-long bonds (e.g. Austria 70y and 100y) have shown strong interest by investors that either try to match long-term liabilities or want to use them as high beta non-derivative speculative instruments on duration risk. Currently there are only EUR13bn worth of bonds outstanding with maturities of +50 years. This market segment surely has more absorption capacity.

The funding structure will set the course for the future of the EU rescue fund. If it is massively financed with ultra-long bonds, it is likely to remain stuck in its embryonic form and become just another player in the already highly fragmented European (quasi-)government bond market. If a more flexible and diversified funding approach is chosen, it could become an active market player with the capacity to contribute to a market harmonization.

Yesterday’s announcement is about much more than the proposed rescue fund. In fact, in its statement, the German-French couple lays out a few moonshots for the European Union. This alignment – particularly at times of subdued market stress – is reassuring. Expect the proposed ideas to feature heavily in Germany’s upcoming EU presidency and beyond. Next to seeking more competences in the area of health policy, the proposal strikes a fine balance between pursuing an ambitious industrial strategy and remaining a champion of open markets and free (but fair) trade, with the fight against climate change, and for more social fairness playing key roles in driving the recovery from the Covid-19 crisis. “Green recovery roadmaps” by sector, higher emission reduction targets coupled with measures and a minimum carbon pricing in the EU ETS are part of the broader ambition, confirming Europe‘s commitment to greening the recovery. With regard to speeding up the digital transformation, the proposal includes the rollout of 5G and a strengthening of cybersecurity, as well as the set-up of an enabling framework for AI, plus fair regulation for digital platforms. On the ambitions to enhance EU economic and industrial resilience and sovereignty and strengthening the single market, the priorities are: supporting the diversification of supply chains, developing an anti-subventions mechanism, ensuring effective reciprocity of public procurement with third countries, setting up a strong non-EU investment screening, encouraging investment (re)location in the EU, a modernization of competition policy, the completion of the EU digital, energy and capital markets, reinforcing social convergence and speeding up the discussion on an EU framework for minimum wages – adapted to national situations.

Domestic and international headwinds: Watch the upcoming EU council for answers. Following the presentation of the Merkel-Macron proposal, the ball is now in the court of the remaining 25 EU members. With time of the essence to ensure that the funds are able to provide the recovery across Europe with sufficient tailwind, a swift agreement is essential. While Italy and Spain have already voiced their support for the rescue fund, Austria together with the Netherlands, Denmark and Sweden gave the idea a lukewarm response - to put it mildly - insisting that any financial support needs to come in the form of loans. Meanwhile the Eastern European EU members are also likely to remain cautious out of fear that the additional burden put on the EU budget could reduce available non-Covid-19 related structural funds. Hence, before we get carried away, there is a sizeable risk that the proposal will need to be watered down to make it palatable for the more skeptical member states. For instance, the distribution key could come under much scrutiny to ensure that net payments are not too focused on a small number of countries but instead more widely shared. The EU Commission’s final proposal is expected on 27 May, which, following a unanimous vote, will also need to be ratified by national governments.